The latest economic and business news during the coronavirus pandemic.

This briefing is no longer being updated. Follow live updates here.

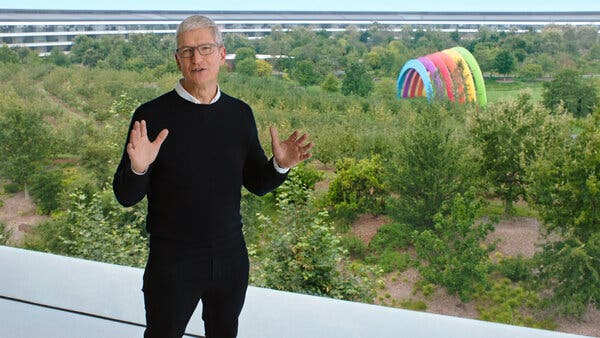

The increasing scrutiny of the biggest tech companies and their ability to quash smaller rivals doesn’t seem to be curbing their ambitions.

Apple said on Tuesday that it would start a new subscription fitness service by year’s end, sending shock waves through a growing industry with dozens of competitors. Companies that sell digital fitness classes have gained new customers since the pandemic closed gyms around the world, but now they have a huge new competitor.

Apple said its Apple Fitness+ service will give users access to digital fitness classes, similar to services from companies like Peloton, Daily Power and CorePower. It costs $10 a month.

Apple also announced a new bundle of its growing list of services, a move that has been expected for more than a year. Apple said there would be various packages available, including its top-tier bundle for $30 a month, which includes access to its music, TV, gaming, news, fitness and cloud services. It’s another example of Apple’s size giving it a major leg up on the competition.

Apple has made its digital-services business the centerpiece of its growth plans in recent years, as sales of the iPhone have largely leveled off. The strategy has worked: Services brought in more $13 billion in the latest quarter, or about 22 percent of Apple’s overall revenue.

But Apple is still focused on being the world’s most profitable hardware business. The company unveiled several more devices on Tuesday, including a $600 iPad Air and a new Apple Watch. The company is expected to release new iPhones next month.

JPMorgan Chase sent some of its workers home this week after an employee in the bank’s trading unit tested positive for the coronavirus, a person familiar with the matter said.

The case was identified earlier this week — around the same time that the bank, which has headquarters in Midtown Manhattan, told some senior employees in its sales and trading division that they would be required to return to the office by Sept. 21, with exceptions for those with child care or medical issues. This employee was not one of those asked to return, and those plans still stand.

As more people return to the office, JPMorgan and many of its Wall Street peers may well have to prepare for the possibility that there will be more frequent instances of coronavirus cases.

“We’ve been managing individual cases across the firm over the course of the last few months and following appropriate protocols when they occur,” a JPMorgan spokesman, Brian Marchiony, said in a statement. He declined to comment on individual cases.

News of the coronavirus case was reported earlier by Bloomberg.

Delta Air Lines has avoided the need to furlough much of its work force in the coming weeks, sparing many employees the fate faced by tens of thousands at other airlines.

The airline’s chief executive, Ed Bastian, made the announcement in a letter to staff members on Tuesday, crediting a range of concessions by Delta employees.

“We had an enormous response to the enhanced early retirement and departure packages that were offered this summer, with 20 percent of our people choosing voluntary exits,” he said. “While it is difficult to see so many of our colleagues leave, every one of those departures helped save Delta jobs.”

More than 40,000 Delta employees volunteered to take short-term or long-term unpaid leaves. The airline also cut hours by 25 percent for many workers.

While Delta’s flight attendants and those who work in customer service, cargo, reservations, airplane maintenance and other areas will be spared, the airline said it would still need to furlough about 2,000 pilots, as previously announced. Delta’s pilots are unionized, while there is a campaign underway to unionize its flight attendants.

American Airlines expects to furlough 19,000 workers starting on Oct. 1, when a ban on broad cuts that was a condition of federal aid expires. United Airlines has said it plans to furlough 16,000. Like Delta, Southwest Airlines has said it will be able to avoid such cuts.

American, United and Delta have said that many jobs under threat could be spared if Congress renews the funding provided under the CARES Act, which passed in March and included $25 billion for passenger airlines to pay employees.

Lawmakers in both parties have expressed support for such funding, but broader talks have been stalled for weeks.

A World Trade Organization panel said Tuesday that the United States violated international trade rules by imposing tariffs on China in 2018 in the midst of President Trump’s trade war.

The panel of trade experts sided with a complaint that had been filed by China, which argued that Mr. Trump’s tariffs violated several global rules, including a provision that requires all W.T.O. members to offer equal tariff rates among the body’s trading partners.

Mr. Trump broke with that tradition. During his trade war with China, the president imposed tariffs on more than $360 billion worth of Chinese products, in an effort to persuade China to strengthen its intellectual property protections and make other changes to policies that Mr. Trump said put American workers at a disadvantage. The administration drew on an American legal provision — called Section 301 — to impose the tariffs, which allows the president to restrict foreign commerce that unfairly burdens the United States.

The impact of the ruling remains unclear. The United States and China signed a trade deal in January, but the bulk of the tariffs imposed by the Trump administration remain in place, covering more than half of China’s exports to the United States.

“This panel report confirms what the Trump administration has been saying for four years: The W.T.O. is completely inadequate to stop China’s harmful technology practices,” Robert E. Lighthizer, the United States trade representative, said in a statement. “Although the panel did not dispute the extensive evidence submitted by the United States of intellectual property theft by China, its decision shows that the W.T.O. provides no remedy for such misconduct.”

August was the busiest month in the 114-year history for the Port of Los Angeles, the nation’s top container port, as retailers restocked depleted warehouse and store shelves and prepared for a holiday surge. But don’t get excited about an economic rebound just yet.

“With all of this, a word of caution: One month or even one quarter does not make a trend,” Gene Seroka, the port’s executive director, told reporters on Tuesday. “Despite this import surge that we’re seeing, the U.S. economy and global trade face significant challenges.”

The high cargo volume in August, an increase of nearly 12 percent over last year, was driven in part by record imports, Mr. Seroka said. He forecast busy months ahead and said the port expected trade volumes to be down only 9 percent for the year, compared with an earlier estimate of 15 percent.

Jonathan Gold, vice president of the National Retail Federation, an industry association, said the port’s data aligned with his group’s findings. Consumer confidence has been rising, he said, as have sales around significant dates and events, including July 4, Mother’s Day, Father’s Day and the return to school.

“We’re hoping that those trends will continue going forward,” he said.

-

Kohl’s said on Tuesday that it cut about 15 percent of corporate positions at the company, as the retailer continued to grapple with fallout from the pandemic. The retailer said the cuts would reduce expenses by $65 million on an annualized basis.

-

The newspaper chain Tribune Publishing is permanently closing the Newport News, Va., newsroom of two of its papers, The Virginian-Pilot and Daily Press. The closure, announced to staff Tuesday in an email from a company executive, follows the shuttering last month of four of Tribune’s other newsrooms, including that of the New York Daily News.

-

The S&P 500 added to its gains this week, rising about half a percent on Tuesday, following global shares higher after some positive economic data out of China.

-

Tech shares rose, pushing the Nasdaq up more than 1 percent. Apple eked out a gain of less than 1 percent after the tech giant announced that it would start a new subscription fitness service by year’s end, joining a growing industry with dozens of competitors.

-

European indexes were all higher, with the FTSE 100 in Britain up more than 1 percent and the Dax in Germany slightly higher. Most Asian markets closed higher; in Hong Kong, the Hang Seng gained 0.4 percent, and in South Korea, the Kospi rose 0.7 percent.

-

Fresh data out of China showed that the country’s economy was beginning to pick up steam. Industrial output rose 5.6 percent in August, the most in eight months, and retail sales grew 0.5 percent from a year ago, for the first time this year.

-

“Strong external demand, a further recovery from the pandemic and pent-up demand from the floods all contributed to the robust activity data in August,” said Ting Lu, chief China economist at Nomura, according to Reuters.

-

Industrial production in the United States rose 0.4 percent in August, data released by the Federal Reserve on Tuesday showed. That’s a much slower pace than in June and July when production rose by 6.1 percent and 3.5 percent.

The Trump administration said Tuesday that it would lift a 10 percent tariff on Canadian aluminum that it announced a little over a month ago after consultations with the Canadian government.

The Office of the United States Trade Representative said that it expected imports of aluminum from Canada to decline in the last four months of 2020, but that if they did not, the United States could retroactively impose its tariffs.

President Trump first placed tariffs on steel and aluminum from Canada, along with Mexico, in 2018. Both countries retaliated against the United States with their own levies, and the United States lifted its tariffs in May 2019.

But in recent months, the administration complained of what it called a surge in imported metal from Canada that was harming American aluminum smelters, and moved to reimpose the levies.

The statement from the Trump administration came as Canadian officials prepared to announce retaliatory tariffs on American products on Tuesday afternoon. In August, the Canadian deputy prime minister, Chrystia Freeland, had said that Ottawa would impose counter tariffs on $2.7 billion worth of American aluminum and aluminum products by Sept. 16.

Lifting the tariffs will remove one impediment to the U.S.-Canada relationship. The Canadian government was particularly angered that the administration said it had imposed the tariffs to safeguard American national security, because Canada is a close military ally.

In lieu of the tariffs, the United States set tight limits on the amount of aluminum that can be imported from Canada. The Office of the United States Trade Representative said it expected Canada to send no more than 83,000 tons of non-alloyed, unwrought aluminum to the United States in September and November and 70,000 tons in October and December.

If actual shipments exceeded 105 percent of those amounts, the United States would retroactively impose a tariff on all shipments made during that month, it said.

Britain’s unemployment rate, which held steady through the early months of the pandemic thanks to the government’s furlough program that keeps people in their jobs, has started to increase.

The rate rose to 4.1 percent for the May-to-July period, the Office for National Statistics said on Tuesday, up from about 3.9 percent. For months, the jobless rate had been held down by the furlough program and by grants for self-employed workers, which “shielded the labor market from the worst consequences of the pandemic,” the statistics agency said.

The ranks of the jobless were also low because many of the people who did lose jobs in the spring were more likely to choose not to look for new work while the economy was in a lockdown, and so were counted as economically inactive.

As the British economy emerged out of lockdown in June and July, some of those people have re-entered the labor market. Although some have found jobs, others have not, helping raise the unemployment rate.

Overall, the agency’s data showed a labor market under the continuing strains of the pandemic.

-

Despite government support programs, in August there were 695,000 fewer payrolled employees than in March, a drop of 2.4 percent.

-

Young people under 25 have been particularly hard hit, continuing to record lower levels of employment as older age groups begin to recover.

-

Layoffs are rising. From May to July, there were 48,000 more redundancies than in the preceding three months, the biggest three-month jump since 2009. There are concerns that this is just the start of a wave of layoffs when the furlough program ends in October. The Institute for Employment Studies estimates there will be 650,000 redundancies in the second half of this year.

The persistently low unemployment rate in Britain stood in contrast to the United States, where the rate climbed above 14 percent in April as people were laid off during the height of state lockdowns and sought government help through unemployment benefits.

Hotel executives — including some of President Trump’s friends and donors — are waging an intense lobbying campaign in hopes of receiving a huge bailout from Washington.

The pandemic has decimated the travel industry, sapping hotels of revenue. As a result, some investors are struggling to make payments on billions of dollars in debt they took on to acquire properties.

Now the executives and their lobbyists are trying to persuade the Trump administration, the Federal Reserve and Congress to rescue hundreds of hotel industry players. Arguing that a bailout will save thousands of jobs and help local economies, they are asking that existing coronavirus relief efforts be extended to the commercial real estate sector, which so far has been cut off from most of the stimulus money.

But industry lobbyists acknowledge that the effort could create the appearance of a conflict of interest for Mr. Trump, who owns his own chain of luxury hotels.

“The idea of bailing out owners of real estate does not even make sense to me,” said Ethan Penner, a real estate investor. “These businesses should be allowed to fail.”

Hotel employees have also argued through their union that rescuing investors who turned to Wall Street to finance hotel buying sprees will not save jobs.

“Jobs are driven by occupancy, and only ending the pandemic can fix that,” said Gwen Mills, the secretary-treasurer of Unite Here, a union that represents 300,000 workers at hotels, casinos, cafeterias and other retail outlets.